Navigating life and disability insurance for Idaho business owners

If you own a business in Idaho Falls, Preston, or anywhere across Eastern Idaho, this question hits home: Can one insurance plan really protect both my business and my family?

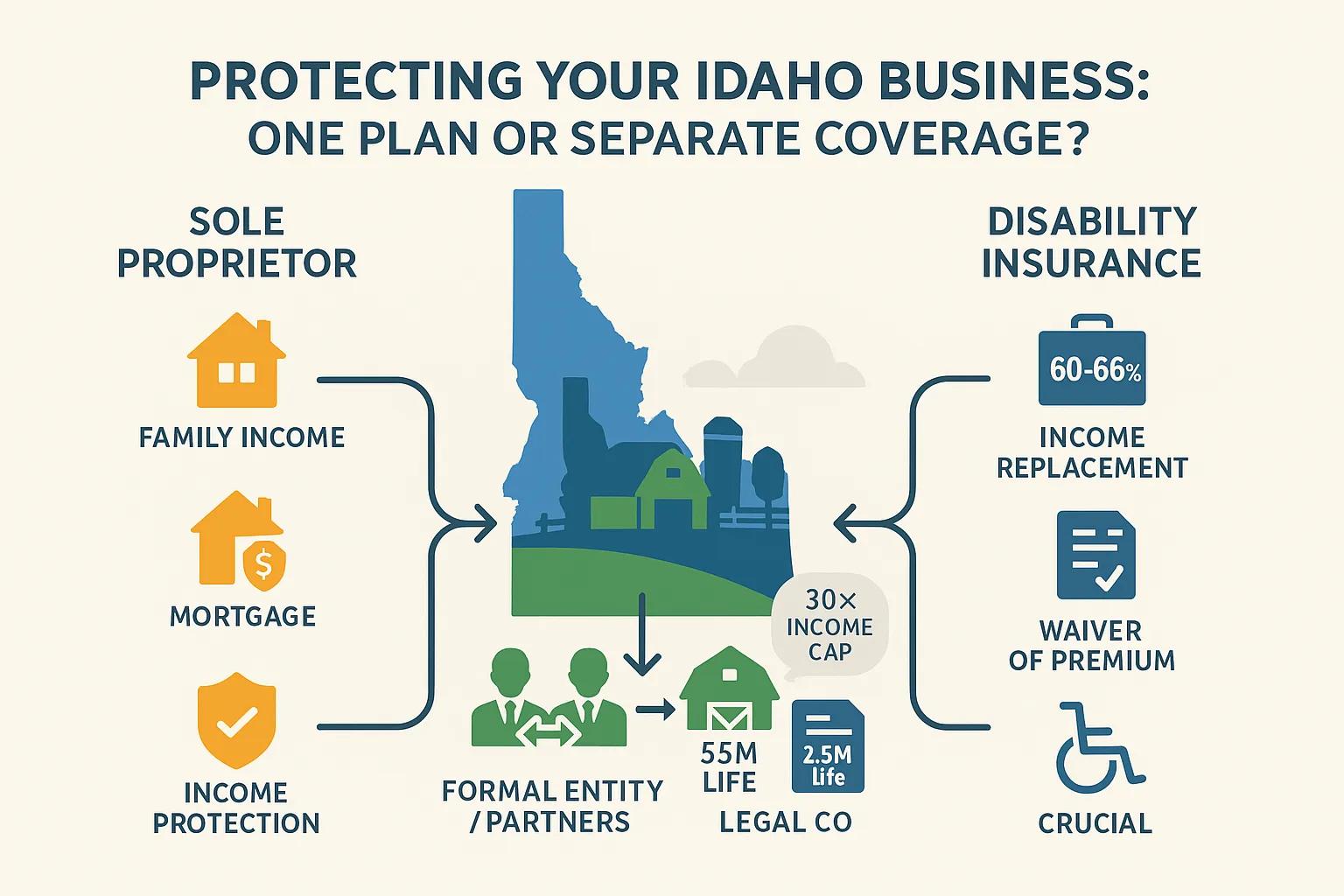

It’s a smart question, and one that requires more than a simple yes or no. For some sole proprietors, one policy may do the job. But for most business owners with partners, formal entities, or growing operations, trying to cram everything into one plan is a risky shortcut.

Let’s break it down based on real scenarios from Idaho business owners, so you can see what’s smart, what’s risky, and how to protect both your family and your company the right way.

What You’re Really Trying to Protect

Most business owners in Idaho Falls and across Eastern Idaho want to protect three things:

- Family income – so your spouse can pay the bills and maintain their lifestyle.

- Major goals and debts – mortgage, vehicles, kids’ college, maybe some retirement protection for a surviving spouse.

- The business itself – so your partner, employees, or farm operation can keep going if something happens to you.

From an insurance standpoint, that means we’re talking about:

- Personal life insurance – to protect your family.

- Business-owned life insurance – to protect the business and/or partners.

- Disability insurance – so you still have income if you’re alive but can’t work.

Trying to use a single plan to solve all three? That’s where many Idaho entrepreneurs get into trouble.

How Much Life Insurance Can You Actually Get?

Most people never hear this part clearly: If you’re in your 30s or 40s and still working, life insurance companies will usually only offer you up to a certain multiple of your income.

- Under age 40, that’s often up to 30× your income.

- Example: If you make $100,000 per year, you might qualify for $3,000,000 of life insurance.

- If you make $150,000, you might qualify for $4.5 million.

Why 30×? Because that amount can typically:

- Provide income for your spouse for the rest of their life

- Cover the mortgage and vehicle loans

- Help pay for kids’ college

- Cover other major family obligations

If you say, “I want $5 or $6 million,” the carrier may say no—because it doesn’t match your income. They’re trying to prevent over-insurance.

So right away, that limits how much “room” you have to use one policy for both family needs and business buyout needs.

When One Policy Might Be Enough

If you’re:

- A sole proprietor (no partners, no formal entity, just you), and

- Your business value is tied directly to you and your income, and

- You’re mainly worried about protecting your family,

then yes, one personally owned life insurance policy might be enough to cover:

- Mortgage

- Cars

- Kids’ education

- Income support for your spouse

In this case, your “business protection” is really just income protection, and that’s what your personal life policy is already doing.

But as soon as you have a more complex setup, things change fast.

When You Absolutely Need Separate Business Coverage

If you have:

- A formal entity (LLC, corporation, etc.), or

- Multiple owners/partners, or

- A business with significant assets or enterprise value

then you’re in buy–sell agreement territory—and one policy will not cut it.

A typical cross-purchase buy–sell for two owners looks like this:

- The business is valued at $5 million.

- There are two partners (say, two brothers on a farm).

- Each owns 50% of the business.

Here’s how we structure it:

- Brother A owns a life insurance policy on Brother B for $2.5 million (half the value).

- Brother B owns a life insurance policy on Brother A for $2.5 million.

- They work with an attorney to draft the buy–sell agreement.

If Brother A dies:

- The policy on him pays $2.5 million to Brother B.

- Brother B uses that money to buy out Brother A’s spouse or family.

- The spouse receives the full, fair value of that half of the farm.

- The business can continue under Brother B’s sole ownership.

That’s not something you can realistically do with one life policy. You need:

- Separate ownership

- Correct beneficiary structure

- Legal documents tying it all together

- Enough coverage to match current business value

And that last part matters: business values change. A good buy–sell setup should be reviewed every 2–3 years to make sure coverage still matches what the company is worth.

Term vs. Permanent Life Insurance for Business Owners

For buy–sell arrangements and business protection, you’ve got two main options:

- Term life insurance (e.g., 20-year term) is often used if you plan to exit the business in a defined period (say 20 years). Term life insurance typically has lower premiums and straightforward coverage.

- Permanent life insurance (whole life, indexed universal life, etc.) You can fund these more heavily, build cash value, and later: Swap policy ownership back to each original insured. Each owner ends up with a personally owned policy and keeps the built-up cash value as part of their retirement strategy.

Either way, this is not a one-size-fits-all online quote situation. It’s planning. And that’s where a local insurance agency in Idaho Falls that understands both family and business planning becomes critical.

Why Disability Insurance Is the Missing Piece

Here’s the nightmare scenario nobody wants to think about:

- You don’t die.

- You just can’t work anymore.

That’s where disability insurance comes in, and it’s often more important than life insurance in terms of actual claims.

In practice:

- I’ve written thousands of life insurance policies.

- I’ve written fewer than 100 disability policies.

- I’ve delivered three life insurance death claims.

- And I have three people on disability claims right now.

When disability hits, the agent suddenly becomes the hero, because that monthly check is what keeps the family and sometimes the business afloat. One client actually called their disability policy their “sugar daddy” because it literally paid the bills when they couldn’t.

Key points on disability insurance:

- Benefits are often 60–66% of your income.

- Carriers will look at two years of tax returns to verify income.

- Blue-collar owners pay more because the risk of disability is higher, but they have the same financial risk if they can’t work.

- Many life policies and disability policies can include a waiver of premium, if you become disabled, your premium is waived, and the coverage continues.

If you’re trying to “cover everything” — mortgage, income, college, retirement — for most business owners the honest answer is: You need both life insurance and disability insurance.

Pro Move: When to Buy Disability Insurance as a Business Owner

Here’s a strategic tip most Idaho business owners never hear: The best time to buy disability insurance is when your income looks the highest on paper.

Why? Because disability benefits are based on verified income, not what you say you make.

Common scenario:

- You’re a business owner.

- You’re minimizing taxable income every year with deductions and write-offs.

- On paper, you don’t look like you make much.

- That severely limits how much disability coverage you can qualify for.

But when you:

- Prepare to buy a house, or

- Show higher income for a mortgage,

that’s when your tax returns actually reflect a stronger income. That is a prime moment to buy your disability policy.

If you’re in Idaho Falls, Rexburg, Preston, or anywhere in Eastern Idaho and you’ve got a strong income year on the books, that’s the time to talk to a local agent about locking in a higher disability benefit while you can.

Key Takeaways

One policy sometimes works if you’re a simple sole proprietor and mostly protecting family income.

- If you have partners or a formal entity, you almost certainly need separate business-owned coverage and a buy–sell agreement.

- Carriers typically allow up to 30× income in life insurance for younger clients, that caps how much you can squeeze into a single policy.

- Real-world buy–sell example: two brothers with a $5M farm use two $2.5M policies plus a legal agreement to protect both the business and the surviving spouse.

- Disability insurance is crucial, especially for business owners, it’s often used more than life insurance in real life.

- Blue-collar owners need it too, even if it costs more; the risk of disability is higher.

- The best time to buy disability insurance is when your income looks highest on paper (for example, before or during a home purchase).

Frequently Asked Questions

1. What factors should I consider when choosing between term and permanent life insurance?

When deciding between term and permanent life insurance, consider your long-term financial goals, budget, and the specific needs of your family and business. Term life insurance is typically more affordable and provides coverage for a set period, making it suitable for temporary needs. In contrast, permanent life insurance offers lifelong coverage and can build cash value over time, which can be beneficial for retirement planning. Assess your current financial situation and future obligations to determine which option aligns best with your objectives.

2. How can I ensure my business is adequately protected in case of my disability?

To ensure your business is protected in the event of your disability, consider obtaining a comprehensive disability insurance policy that covers a significant portion of your income. Additionally, establish a business continuity plan that outlines how operations will continue in your absence. This may include delegating responsibilities to trusted employees or partners. Regularly review and update your insurance coverage and business plan to adapt to any changes in your business structure or personal circumstances.

3. What is a buy-sell agreement, and why is it important for business partners?

A buy-sell agreement is a legally binding contract between business partners that outlines how ownership interests will be transferred in the event of a partner’s death, disability, or departure. This agreement is crucial as it ensures that the remaining partners can buy out the departing partner’s share, maintaining business continuity and preventing disputes. It also provides financial security for the departing partner’s family, ensuring they receive fair compensation for their share of the business.

4. How often should I review my life and disability insurance policies?

It is advisable to review your life and disability insurance policies every 2 to 3 years or whenever there are significant life changes, such as marriage, the birth of a child, or changes in business structure. Regular reviews help ensure that your coverage aligns with your current financial situation, family needs, and business obligations. Additionally, as your business grows or your income changes, you may need to adjust your coverage amounts to adequately protect your family and business interests.

5. Can I combine personal and business insurance policies?

While it is possible to combine personal and business insurance policies, it is generally not recommended due to the complexity of coverage needs. Personal life insurance typically focuses on family income protection, while business insurance addresses the unique risks associated with business operations. Combining them can lead to inadequate coverage for both areas. It is often more effective to maintain separate policies tailored to each need, ensuring comprehensive protection for both your family and your business.

6. What are the common misconceptions about disability insurance?

One common misconception about disability insurance is that it is only necessary for physically demanding jobs. In reality, anyone can become disabled due to illness or injury, regardless of their occupation. Another misconception is that disability insurance is too expensive; however, the cost can vary significantly based on factors like age, health, and occupation. Many business owners underestimate the financial impact of a disability, making it crucial to understand the importance of having adequate coverage to protect income and business operations.

7. How does my income affect the amount of disability insurance I can obtain?

Your income plays a critical role in determining the amount of disability insurance you can qualify for, as benefits are typically based on a percentage of your verified income. Insurers often require documentation, such as tax returns, to assess your earnings. If you have a lower reported income due to deductions or write-offs, it may limit your coverage options. Therefore, it is advisable to secure disability insurance during a period of higher income to maximize your potential benefits.

If you’re an Idaho business owner and you’re not sure whether your current setup truly protects both your family and your company, now is the time to find out.

Eagle Cap Insurance works with business owners in Idaho Falls, Preston, and across Eastern Idaho to structure:

- Personal life insurance

- Business-owned life insurance and buy–sell funding

- Disability coverage for owners, especially blue-collar

Schedule a Free Review

We’ll walk through your income, business structure, and goals—and give you a clear, no-pressure plan to protect what matters most.

Author

Kyle Bennett, Founder & Insurance Advisor – Eagle Cap Insurance

20 years in business strategy | 20+ years specialising in life, disability & mortgage-protection planning for Idaho families and business owners.