Mortgage Protection and Life Insurance in Idaho Falls from $50/MonthLife Insurance Idaho Falls: How to Protect Your Mortgage and Family on a $50/Month

Affordable Protection for Idaho Families Starts Here

When most Idaho Falls homeowners hear “life insurance”, they picture something complicated or expensive, the kind of thing you’ll “get to later.” But here’s the truth: many Idaho families protect their entire mortgage and their family’s income for about $50 a month.

At Eagle Cap Insurance, we see it every week. Families come in thinking coverage will cost hundreds, only to learn they can secure $250,000 to $500,000 in protection for less than the cost of one dinner date.

Let’s break down what that actually looks like, and how to make sure your coverage works for your mortgage, budget, and family.

1. The $50 Question: “Is Life Insurance Really Affordable?”

Life insurance doesn’t have to drain your wallet. For most Idaho residents in their 30s or 40s, a $50/month term policy can provide $400,000–$600,000 in coverage, enough to fully protect a home and replace several years of income.

In Idaho Falls, where the average home value sits around $385,000, that amount covers the entire mortgage and then some.

According to the Idaho Department of Insurance, more than 65 percent of insured Idaho households hold a term-life plan under $75/month, proving affordable coverage is the local norm, not the exception.

So yes, life insurance really can fit inside a $50 budget if it’s structured right.

1.1 What Drives Life Insurance Pricing in Idaho? (Idaho-Specific Breakdown)

Life insurance pricing in Idaho follows the same national underwriting rules, but several Idaho-specific factors make coverage more affordable compared with nearby Western states:

• Lower average age of homeowners

Idaho has one of the youngest homeowner populations in the region (median age 36.9), which lowers policy pricing because age is the strongest predictor of term-life cost.

• Lower statewide tobacco use

Idaho’s adult smoking rate sits below the national average, allowing more residents to qualify for Preferred or Super Preferred health classes, reducing premiums by 20–35%.

• Fewer high-risk urban zones

States with large metro concentrations see higher pricing due to health-risk density. Idaho Falls and surrounding Bonneville County carry lower actuarial risk than major metro markets, which supports lower term-life averages.

• High rate of mortgage uptake

Idaho’s homeownership rate is above the U.S. average, which increases demand for mortgage-protection term life policies, leading carriers to offer competitive pricing in the state.

What this means:

A $50 monthly budget stretches further in Idaho than in most Western markets because Idaho homeowners fit more Preferred-rate underwriting profiles.

2. What That $50/Month Actually Covers

Let’s put real numbers on the table.

A 35-year-old non-smoker in Idaho Falls can typically qualify for:

- $250,000 Term Life Policy — $22–$28/month

- $500,000 Term Life Policy — $38–$52/month

- $750,000 Term Life Policy — $65–$75/month

That’s less than most families spend on streaming subscriptions.

Term life policies are straightforward; you pay a fixed premium for 20 or 30 years, and your loved ones receive a tax-free payout if something happens to you during that time.

National carriers list Idaho’s average term-life rate 12–15 percent lower than the U.S. average, thanks to the state’s lower health-risk and claim ratios, meaning your $50 goes further here than in most markets.

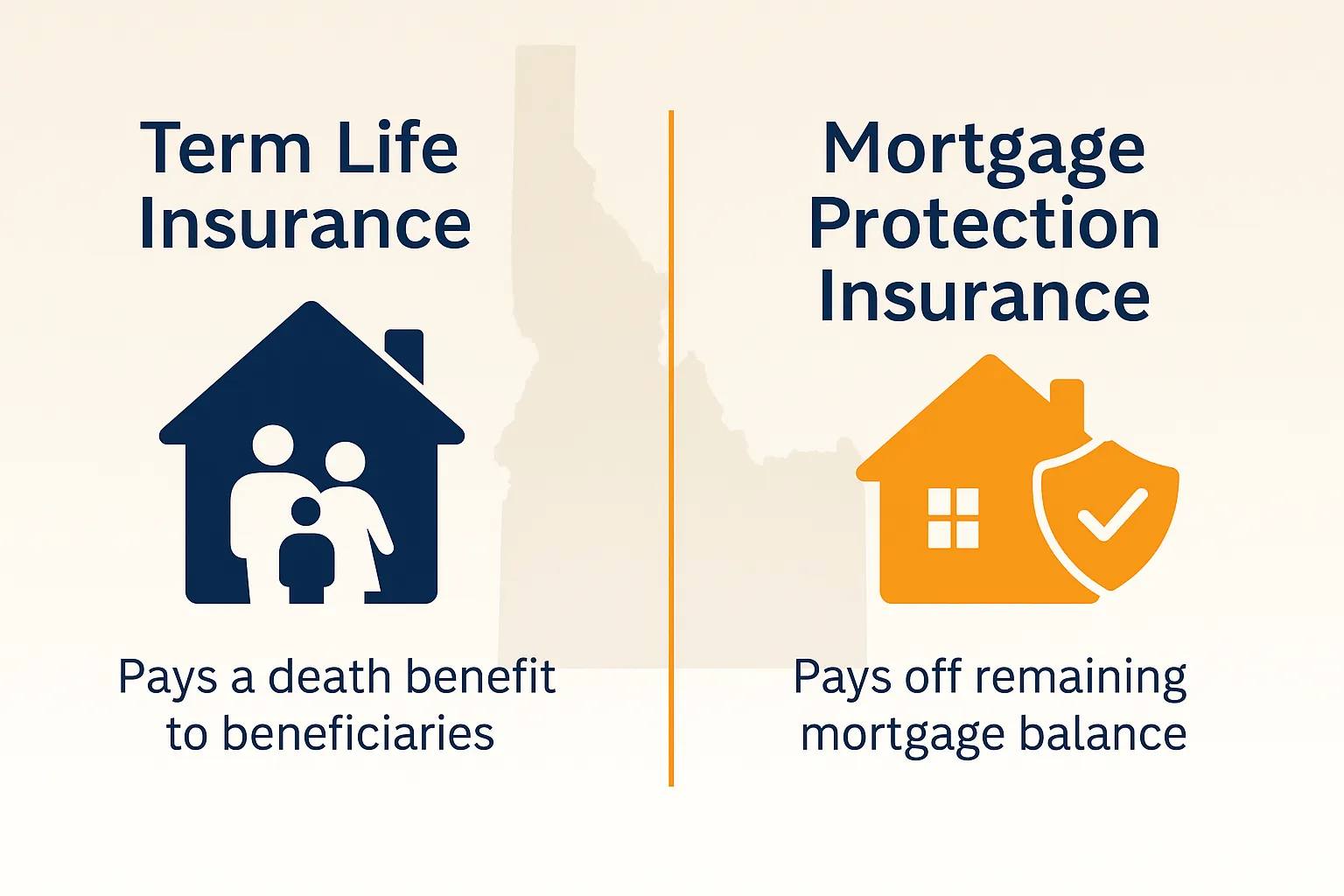

3. Mortgage Protection Insurance vs. Traditional Life Insurance

Both options safeguard your home, but they work differently:

- Mortgage Protection Insurance pays your lender directly. It ensures the house is paid off if you pass away during your loan term.

- Traditional Term Life Insurance pays your family, not the bank. They decide whether to pay the mortgage, clear debts, or invest for future income.

In Idaho Falls, where average monthly mortgage payments run about $2,200, a $400,000 term policy could pay off that loan entirely, giving your family financial freedom, not foreclosure stress.

“Mortgage protection isn’t just about the house,” explainsKyle Bennett

, founder of Eagle Cap Insurance. “It’s about making sure your family keeps the life you built, without starting over.”

3.1 Why Idaho Lenders Push Mortgage Protection Insurance

Many Idaho lenders promote MPI (Mortgage Protection Insurance) at closing because:

- It reduces their risk on newly issued home loans

- It protects lender balance sheets in the first 5–10 years of amortization

- It prevents default during the high-risk early years

But MPI does not protect your family, only the bank.

4. Real Idaho Numbers: Cost-to-Coverage Comparison

That $50 policy can erase a 30-year mortgage, leaving your family with a paid-off home and no lender letters arriving at the worst possible time.

Based on 2024 Idaho Housing Report figures, mortgage protection through term life saves the average household $3,000–$4,000 in annual interest payments when compared with loan-specific insurance from lenders.

5. What Idaho Families Actually Buy

Most families we meet in Idaho Falls choose 20- to 30-year term life policies between $250,000 and $750,000 in coverage. That’s enough to pay the mortgage, clear vehicle or credit-card debt, and fund children’s education.

“For most Idaho Falls families, $40–$60 a month replaces a mortgage, pays off debt, and protects college savings,” saysKyle Bennett

. “It’s about giving your loved ones time, not bills.”

5.1 What Idaho Homeowners Ask Before Buying Life Insurance

Kyle hears the same five questions from Idaho Falls and Preston homeowners:

- “How much coverage protects my entire mortgage?”

- “Should I match my policy length to my loan term?”

- “Is $50 really enough if I have kids?”

- “What’s the difference between a Preferred and Standard rate?”

- “Does life insurance go up if Idaho housing prices rise?”

6. The Advisor’s Take: Building Protection That Fits Your Life

Kyle’s approach is simple: align protection with what matters most, not what costs the most.

He walks Idaho homeowners through income, mortgage balance, dependents, and future goals to tailor a plan that feels realistic.

Affordable life insurance isn’t about paying less; it’s about structuring smarter.

7. Real Coverage for Real Budgets

If you own a home in Idaho Falls, protecting it doesn’t have to break your budget.

A $50/month policy can secure your home, protect your spouse’s income, and keep your kids’ college plans intact, even when life doesn’t go according to plan.

At Eagle Cap Insurance, we simplify life insurance so you can make confident, informed decisions that fit both your family and your finances.

👉 Schedule a free 15-minute consultation with Kyle: Book Here

Author

Kyle Bennett, Founder & Insurance Advisor – Eagle Cap Insurance

20 years in business strategy | 20+ years specialising in life, disability & mortgage-protection planning for Idaho families and business owners.