How Disability Insurance Protects Idaho’s Small Business IncomeDisability Insurance in Idaho: What Small Business Owners Need Before an Injury Happens

Protecting Your Income Isn’t Optional. It’s Survival.

Most business owners in Idaho know how to hustle. They’re the first ones in, last ones out, often running the business around the clock. But what happens if you can’t work tomorrow?

For many, the answer is silence, and bills that don’t stop.

A back injury, illness, or even a simple accident can sideline a business owner for weeks or months. Without income protection, that “short break” could cost thousands in lost revenue, unpaid overhead, or even lost clients.

At Eagle Cap Insurance, we help Idaho entrepreneurs, contractors, and self-employed professionals protect the income their families and businesses rely on every single month.

1. The Hidden Risk for Idaho Business Owners

When people hear “disability insurance,” they often think of workplace coverage or state programs. But for small business owners, especially those who are self-employed or run LLCs, that safety net rarely exists.

Idaho does not offer a state disability insurance program, leaving self-employed professionals entirely responsible for replacing lost income. According to the Idaho Department of Labor, small businesses employ nearly 56% of the state’s private workforce, which means when an owner is out, so are dozens of local paychecks.

According to the Idaho Department of Insurance, fewer than one in four self-employed Idahoans currently have any form of disability or income protection coverage, leaving more than 120,000 local professionals financially exposed if they can’t work.

Here’s what that looks like in real life:

A contractor in Idaho Falls slipped on an icy driveway last winter and fractured his ankle. He was out for six weeks—no income, no workers’ comp, and no safety net.

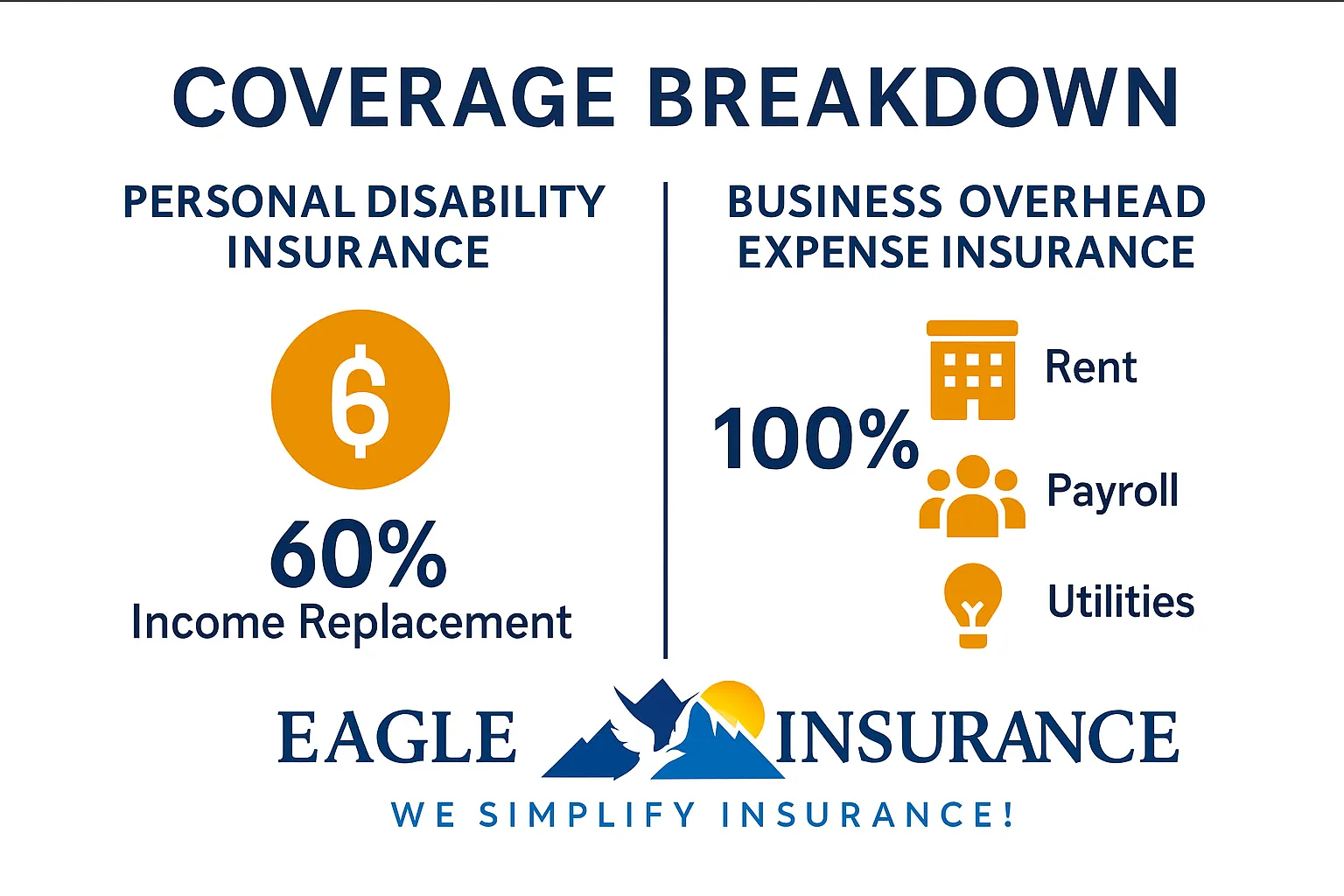

If he’d had disability insurance, it could have replaced up to 60–70% of his income, covering mortgage, utilities, and loan payments while he recovered.

That’s why business disability insurance in Idaho isn’t just another policy, it’s a lifeline.

2. What Disability Insurance Really Covers (And Why It’s Misunderstood)

Disability insurance replaces part of your income when you can’t work due to illness or injury. It doesn’t require an on-the-job accident, it applies whether you’re injured skiing at Teton Pass or diagnosed with a chronic illness that prevents you from working.

There are two main types:

- Short-term disability insurance covers immediate needs (usually up to 3–6 months).

- Long-term disability insurance covers extended recovery or permanent loss of income potential.

And for small business owners, there’s a crucial third option: Business Overhead Expense (BOE) insurance.

BOE doesn’t replace your personal income. It covers operating expenses, the bills your business can’t pause:

- Office rent

- Utilities

- Payroll

- Equipment leases

- Insurance premiums

An Idaho Falls dental practice owner used BOE coverage to keep paying $7,000 in monthly office costs during shoulder surgery recovery. His patients stayed, his staff stayed, and his practice didn’t lose traction.

For most Idaho families, losing just one month of income can eliminate nearly 80% of their household savings, according to regional financial stability studies. That’s why early planning for income protection isn’t a luxury, it’s essential.

3. How Disability Insurance Keeps Idaho Businesses Afloat

Without coverage, even one missed paycheck can start a financial chain reaction.

According to 2025 BLS data, fewer than 4 in 10 private-sector employees have long-term disability coverage, and small employers are least likely to offer it, meaning most Idaho business owners have no formal income-replacement plan unless they purchase it privately.”

Here’s what business disability insurance can protect:

- Your household income — covering personal bills while you recover.

- Your business operations — covering rent, loans, and payroll through BOE coverage.

- Your employees and clients — ensuring your business doesn’t shut down while you’re out.

Think of it as continuity insurance for your life and work. When you’re healthy, it feels optional. When you’re hurt, it’s the only thing that keeps your business alive.

While the national average for short-term disability benefits replaces about 60% of lost income, Idaho-based private plans average 65–70% replacement, thanks to the state’s lower premium-to-benefit ratio; that extra 10% can be the difference between staying open and shutting down.

(Sources: Employee Benefits Survey 2025; Social Security Administration Actuarial Publication No. 2024-01.)

4. Which Idaho Industries Are Most at Risk?

Specific industries in Idaho see higher rates of disability claims due to physical labor or specialized skills.

Idaho’s 2023 Census of Fatal Occupational Injuries shows Transportation and Material Moving as the leading category for serious incidents, followed by Construction and Agriculture. Federal BLS data confirm those same sectors carry the nation’s highest long-term disability claim rates.

- Construction and skilled trades

- Real estate professionals and brokers

- Dentists, chiropractors, and medical practitioners

- Agricultural and ranching operators

- Self-employed consultants and accountants

These professions rely on active, hands-on work. If the person behind the business goes down, revenue does too.

The Idaho Small Business Development Center estimates that over 40% of small businesses would permanently close within three months if the owner became unable to work without disability coverage in place.

Source: Idaho Department of Labor / BLS — Fatal occupational injuries in Idaho 2023

↳

5. Self-Employed or LLC Partner? Here’s What You Need Before It’s Too Late

If you’re self-employed, no one is paying you if you can’t work. That means you are your income source, and protecting it is just as important as protecting your tools, your truck, or your office space.

Here’s what Idaho self-employed professionals should consider:

- Start early — The best rates come while you’re healthy. Waiting until after an injury or diagnosis can disqualify you.

- Customize coverage — Not all policies are alike. Kyle helps clients choose between personal income replacement, overhead coverage, or both.

- Integrate with your business plan — If you have a partner, consider a Buy-Sell Agreement funded by disability insurance to protect both owners in case one can’t return to work.

A Preston-based electrician once told us, “I insured my van before I insured myself.”

That’s the mindset shift disability coverage creates—it protects you, not just your assets.

In Eagle Cap’s experience, many Idaho business owners can secure starter disability coverage for roughly 1%–3% of their monthly income, depending on age, health, and occupation class. For some professionals, that means entry-level policies starting around $75–$120 per month, while higher-risk trades may pay more.

The Advisor’s Take: Why Timing Is Everything

Here’s what Kyle Bennett, founder of Eagle Cap Insurance, tells every business owner:

“Most people call me after the injury, not before. Disability coverage only works if you have it in place before life happens.”

It’s an uncomfortable truth, insurance can’t retroactively protect you. But setting it up now can mean the difference between recovery with peace of mind and recovery with financial panic.

Kyle’s approach is simple: He walks Idaho business owners through exactly what their income, expenses, and dependents look like, and builds a plan around those numbers, not assumptions.

That’s why Eagle Cap clients often say the same thing: they didn’t just get a policy; they got a strategy.

Protect Your Income Before It’s Interrupted

You’ve built a business around reliability. Your clients depend on you. Your family depends on your income.

Now it’s time to protect it.

Whether you’re a small business owner, self-employed, or part of a growing LLC, disability insurance in Idaho gives you control when life throws you off balance.

At Eagle Cap Insurance, we help you integrate disability, life, and business insurance into one cohesive plan—so if something happens, your business and family stay secure.

Or schedule a quick call with Kyle to find the right coverage for you:

Book a free 15-min consultation

Author:

Kyle Bennett, Founder & Insurance Advisor – Eagle Cap Insurance

20+ years in business strategy, 10+ years specializing in income protection and insurance planning for Idaho business owners.